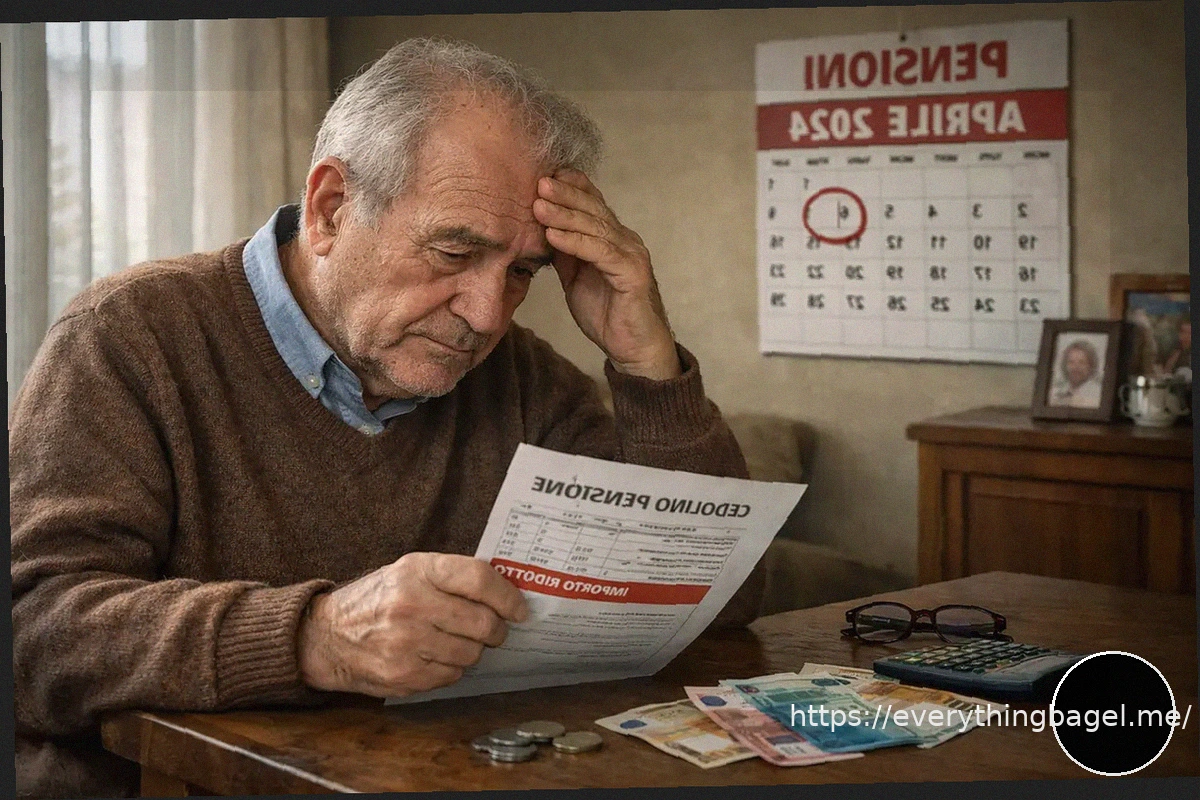

Significant adjustments to pension payments are set to affect many Italian beneficiaries starting in April. These changes involve revised payment schedules, new rules for cash withdrawals, and crucial technical recalculations by INPS (Italy’s National Institute for Social Security). This article delves into the various impacts these new regulations and error corrections will have on monthly pension benefits, potentially leading to lower perceived or actual payments for a considerable number of pensioners.

Payment Dates and Collection Procedures

The pension payment calendar is a vital reference for many Italian citizens, and any shifts in accreditation dates can significantly influence daily financial management. For April, pension benefits will be disbursed starting on the first working day of the month, which is a Wednesday. This timing aims to prevent delays often caused by holidays or weekends disrupting financial transfers.

For pensioners who receive their benefits through post offices, a staggered collection schedule based on the initial letter of their surname is suggested. While not strictly mandatory, this system is designed to reduce queues and waiting times at offices. Poste Italiane utilizes this approach to enhance service efficiency, with specific days allocated for different surname groups throughout the week. This logistical organization helps streamline the withdrawal process, particularly in busy urban areas, making it more orderly and manageable.

Cash Withdrawal Regulations

Cash withdrawal of pensions remains a preferred method for many beneficiaries within the Italian pension system, but it now comes with specific procedural particularities. Current regulations permit cash withdrawals only for amounts not exceeding €1,000. Beneficiaries receiving larger sums are required to opt for direct crediting to a bank or postal current account. This measure aims to reduce the use of cash and encourage transaction traceability.

To avoid lengthy queues and simplify withdrawals, individuals with a Savings Book, a BancoPosta account, or a Postepay Evolution card with advanced banking features are encouraged to use ATM terminals. Postamat machines, typically located outside post offices, offer convenient 24/7 withdrawal services. The shift towards digital tools reflects a broader cultural transformation, influencing how pensioners manage their monthly income. However, some elderly individuals still show resistance to change, due to familiarity with cash and trust in traditional methods. This transition dynamic is crucial for understanding the future adaptation of the pension system.

Changes and Potential Reductions in Benefits

In the current economic climate, the net value of pension benefits can fluctuate due to various legislative and fiscal factors. A primary cause of net amount reduction stems from regional and municipal IRPEF (personal income tax) surcharges, which are divided and included in payment slips from March to November. This spreading helps pensioners avoid large deductions concentrated in single months.

Furthermore, many pensioners observed an increase in their March payment due to the inclusion of arrears for social increases, totaling approximately €60, which also covered the first two months of the year. However, from April onwards, beneficiaries will only receive the standard current quota of €20, leading to a perceived reduction compared to the previous month. This complex system of pension disbursement, involving periodic adjustments and corrections, mirrors the intricate nature of Italian pension regulations, where income stability can be perceived as uncertain by beneficiaries. It is crucial for pensioners to stay informed through official channels for a precise understanding of the mechanisms determining their monthly payment.

Technical Recalculations and Payment Impacts

A significant source of variation in pension disbursements involves a technical recalculation undertaken by INPS. Recently, the institute identified procedural errors in tax deduction calculations from the previous year. Approximately 15,000 pensioners mistakenly benefited from deductions exclusively intended for active workers, leading them to receive sums that now require recovery.

The management of these rectifications is a complex procedure involving cross-analysis and record verification. The errors resulted from incorrect fiscal deductions applied to pensioners with annual incomes between €20,000 and €40,000. This led to an asymmetry that allowed for surplus monthly payments, in some cases up to €1,000 in excess. The review and recovery of these sums constitute a process that is not only technical but also political, considering the necessary balance between fiscal justice and the impact on individuals. For those affected, INPS has arranged for the recovery of sums through monthly deductions, potentially spread over time to avoid excessive reduction of the perceived monthly amount. This approach is designed to safeguard pensioners with lower incomes, preventing drastic decreases through installment plans that allow for a gentler repayment.

Measures for Recovering Unduly Paid Sums

The process of returning unduly received sums is carefully orchestrated by INPS to limit the financial impact on pensioners. Recoveries do not require active intervention from those concerned, as the amounts are directly reduced from the monthly pension payment. This compensation mechanism is precisely calibrated to prevent pensioners with lower incomes from experiencing zeroed-out benefits.

Specifically, the social security institute has established an installment system that distributes the debt over several months, ensuring that each monthly deduction is manageable and compatible with the daily economic needs of the affected beneficiaries. The scheduling of recoveries considers different income situations, allowing for flexibility that does not unduly burden the household budgets of pensioners affected by the calculation error. For transparency and clarity, every pensioner can access their profile on MyINPS online, where they can find detailed information on expected deductions and repayment methods. This accessibility to information allows each pensioner to best plan their finances, a right to information that proves fundamental in ensuring trust and understanding of the social security institution’s initiatives.

Effects of Recent Pension Increases

In recent months, the landscape of Italian pensions has benefited from compensatory and institutional increases that, although modest, represent an important lightening of the fiscal burden for many. Currently, an annual revaluation of 1.4% is active, which leads to a progressive increase in pension amounts, keeping them aligned with inflation and preserving pensioners’ purchasing power.

Among the measures adopted, there is also a reduction in the IRPEF rate from 35% to 33% for intermediate incomes, specifically between €28,000 and €50,000. This reduction has a concrete impact on the net amount received, especially for pensioners in this income bracket who will see a slight but significant difference in their monthly budget. These modifications, introduced as part of broader fiscal and social security reform strategies, aim to alleviate some of the economic pressures that pensioners face daily.