Poste Italiane savings bonds (buoni fruttiferi) are among the most popular and secure savings instruments in the Italian financial landscape. However, many people are unaware of their true net returns. These instruments, guaranteed by the State through Cassa Depositi e Prestiti, are a preferred choice for those looking to protect their capital without excessive risk. But what is the actual yield of these bonds, especially when held for four years? And how do they compare to other investment options such as BTPs (Italian Treasury Bonds) or fixed-term deposit accounts?

How Poste Italiane Savings Bonds Work

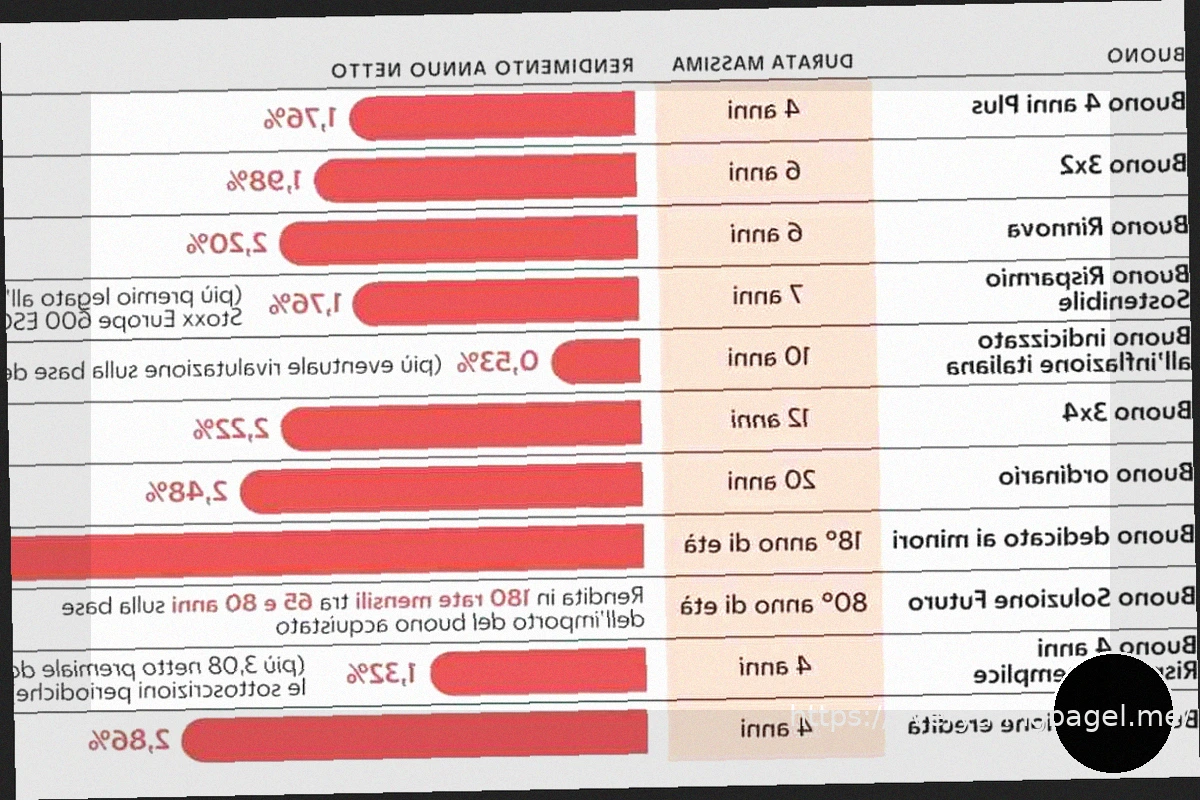

Savings bonds are investment instruments characterized by varying maturities and yields. They are always state-guaranteed and subject to a favorable tax rate of 12.5%, similar to government bonds. They have no subscription or redemption fees and are exempt from inheritance tax. They can be purchased with amounts starting from 50 euros and are available in various types and durations, including the four-year option.

For example, the “4-year plus” savings bond offers a gross annual yield of 1.4%. This means that, on an initial investment of 10,000 euros, a total amount of 10,500 euros would be returned at maturity.

A distinctive advantage of savings bonds over BTPs is the ability to always liquidate the investment “at par.” This implies that, in case of sudden need, it is possible to withdraw the initial capital without risk of loss on the capital itself, although any accrued interest would be forfeited. This characteristic makes savings bonds ideal for those who prioritize security and immediate liquidity, even if it means accepting a more modest return.

In contrast, four-year BTPs tend to offer significantly higher yields, almost double that of savings bonds. For an investment of 10,000 euros, the final return could be around 10,916 euros. However, selling BTPs before maturity exposes investors to greater risks, as their market price can fluctuate based on interest rates and general economic conditions.

Savings Bonds vs. BTPs: A Guide to Choosing for Profit and Security

The difference in yield between savings bonds and BTPs is clear, but it is justified by the differing nature of risk and liquidity. Savings bonds guarantee immediate liquidity and protected capital in exchange for a lower return. BTPs, on the other hand, require more careful planning and greater awareness of risks, as early sale may result in losses or lower-than-expected gains.

For those with small savings who prefer a risk-free option, the savings bond is the better choice. Those with larger assets who can tolerate market fluctuations might find BTPs more advantageous due to their higher yields.

While savings bonds and BTPs are considered relatively secure instruments, fixed-term deposit accounts present some additional risks. Although some deposit accounts currently offer competitive returns (e.g., up to 2.59% net), it is crucial to consider the risk associated with the issuing institution and the lack of liquidity during the fixed term. Beyond the 100,000 euro threshold, deposited funds are no longer guaranteed by the Interbank Deposit Protection Fund, and a long-term lock-up can create problems for those who need to access their funds.